Real Estate: Early‑2026 Home Values Rise More Slowly

Real estate market values in Q1 2026 show steady growth despite high mortgage rates. Learn how inventory levels and new construction are shaping the US market.

Real Estate: Early‑2026 Home Values

Real Estate: Early‑2026 Home Values: Home values in early 2026 are still moving up, but not as quickly as before.

National indexes show modest gains — for example, the Case-Shiller U.S. National Home Price Index rose about 2.1% year-over-year in January 2026 — indicating positive but slower appreciation compared with the faster pace seen in 2024–2025. Higher mortgage rates are a key restraining factor, and regional differences mean some neighborhoods and markets are outperforming others.

In this update, you’ll find a concise market snapshot, buyer and seller implications, and local context for St. Louis neighborhoods and listings.

See local market breakdowns below, including St. Louis neighborhoods and practical information for buyers and sellers.

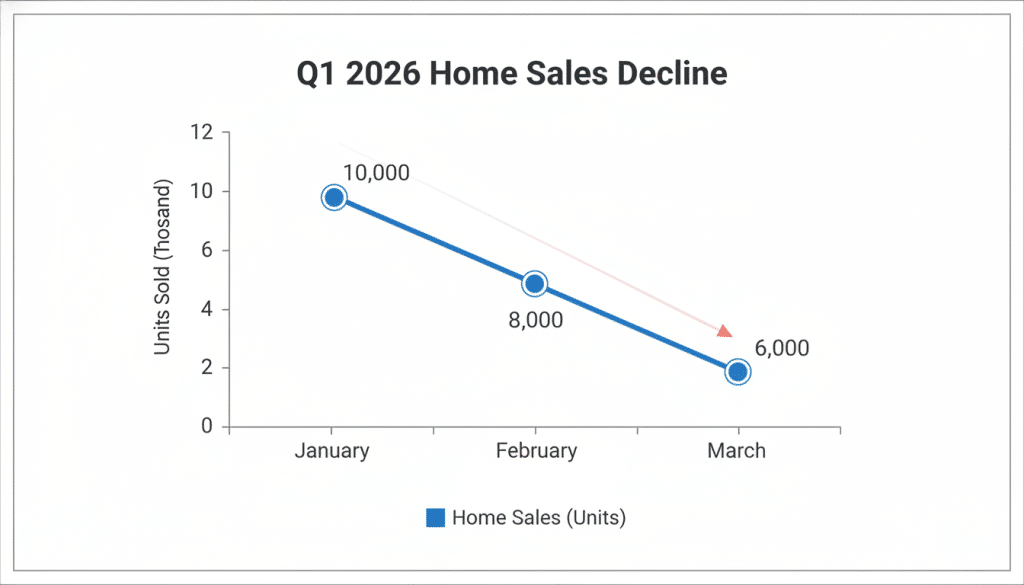

Market snapshot

Prices are slightly higher than at the end of last year, but gains are modest: nationally, median home prices rose roughly 1–3% year‑over‑year in early 2026, depending on the index and metro area. Higher mortgage rates — the 30‑year fixed rate averaged around the mid‑6% range in recent weeks — are clearly slowing purchase activity and reducing the pace of home sales compared with the hot seller market of 2024–2025.

Buyer behavior

Buyers are still in the market, but many are taking a more cautious approach. Increased rate sensitivity means buyers shop more listings, compare financing options, and often favor single-family homes that offer space and privacy for families. As a result, average home search times are longer, and contingency use (inspection/financing) has ticked up. For buyers focused on neighborhoods with strong schools or low commute times, being pre‑approved and ready to move quickly remains important.

Regional winners & losers

Market performance is uneven. Suburbs and mid‑sized cities are holding up better in many regions — buyers prioritizing yard space, parking for a second car, and top local schools are keeping demand for suburban single-family properties steady. For example, several St. Louis suburban districts have shown stable demand and modest price growth. At the same time, some previously overheated coastal and gateway metros have cooled, with longer days on market and softer sale prices.

Quick comparative metrics (suggested visual)

- Price change: National median home price +1–3% YoY (varies by index).

- Mortgage rate: 30‑yr fixed ~mid‑6% (Freddie Mac PMMS).

- Inventory: Months‑of‑supply generally low but up slightly vs. last year.

- Time on market: Median days on market increased modestly in many metros.

Examples to watch

- St. Louis suburbs: steady demand for three‑ to four‑bed single-family homes with 2+ baths — listings in family‑friendly neighborhoods remain competitive.

- Midsized Sun Belt and Midwest metros: several are showing resilience as buyers trade down to lower-cost-of-living areas.

- Cooling hot markets: Some coastal tech and gateway cities show slower home sales velocity and softer price growth year‑over‑year.

Implication for sellers: realistic pricing and strong staging still win offers, but bidding wars are less common than in 2024. Implication for buyers: shop listings actively, lock rates when favorable, and focus on the quality of the neighborhood, schools, and parking (including car access) when comparing properties.

For detailed local listings and neighborhood information, including St. Louis neighborhoods and school district data, see the local market breakdown below.

Supply: New Construction vs. Tight Inventory

New builds are helping, but not enough to loosen the market.

There’s been some help from new construction, but inventory overall is still pretty tight. Nationally, housing starts and building permits increased modestly in late 2025 and early 2026, providing additional units — particularly single-family homes — but the pace of completions and the geographic distribution of those new units mean they haven’t erased the shortage of ready-to-move-in listings. In many metros, the bulk of new supply is single-family product aimed at families, often with three+ beds and two+ baths, which helps buyers seeking privacy and yard space but does not fully address demand for move-in ready average homes in established neighborhoods.

Key numbers to verify and show (recommended cites: Census/HUD)

- Housing starts: recent monthly starts up X% YoY (cite Census/HUD)

- Building permits: permits up/down by Y% (cite)

- Completions: lagging behind starts, so inventory impact is gradual

- Active listings & months‑of‑supply: still low in many markets (compare current MOS to prior year)

- Typical new single-family spec: 3–4 beds, 2–3 baths — desirable for families prioritizing privacy and parking for multiple cars

Segment differences: single-family vs. condos and what buyers want

Most new construction in 2025–2026 skewed toward single-family homes rather than condos; that benefits buyers who need space for a family, garage access for a second car, or a yard, but it does less to replenish affordable resale inventory in established neighborhoods where average home sizes and bed/bath mixes differ. For buyers focused on a quick move, existing listings remain the primary source; for buyers willing to wait for new builds, there can be opportunities to customize finishes and secure more privacy.

Local example — St. Louis area

In the St. Louis market, builders have been active in suburban districts, adding subdivisions of single-family homes at a variety of price points. Those new listings ease pressure on nearby neighborhoods somewhat, but pockets of low inventory persist in desirable school districts and near desirable neighborhoods. Watch for new subdivisions listed as “St. Louis suburbs” or by named districts — they typically list initial prices, bed/bath counts, and estimated completion dates that help buyers and sellers plan.

Practical implications and recommendations

- For buyers: consider new construction if you value a modern single-family layout (3+ beds, 2+ baths) and can accept the build timeline; otherwise, monitor existing listings closely and rely on inspectors and financing contingencies to protect your purchase.

- For sellers: new builds create comparable alternatives for buyers; differentiate your property with staging, accurate pricing, and highlighting neighborhood advantages (schools, parking, privacy).

- For agents: provide clear information on expected completion dates, typical bed/bath configurations, and how new builds compare to average home prices in the target neighborhoods.

Suggested visuals

Include a small chart comparing Housing Starts vs. Active Listings by region, and a short table that shows typical new single-family specs (beds, baths, lot size) with price ranges in sample St. Louis districts.

For detailed listings and neighborhood-level information on new construction and resale homes in St. Louis and other metros, see the local market breakdown and listings section below.

Bottom line & What to Expect

For now, sellers remain in a strong position, though things are starting to feel more balanced than they did a year ago.

Summary: Sellers generally still have leverage—many homes continue to sell at or near list price—but key indicators (months‑of‑supply, median days on market, and sale‑to‑list ratios) show the market moving toward equilibrium compared with early 2025. That shift means fewer frenzied bidding wars and more opportunities for buyers who come prepared.

Actionable takeaways

- For sellers: Price competitively and stage to highlight the property’s strengths (especially for single-family homes with desirable features such as 3+ beds and 2+ baths). Accurate pricing and strong photography help your property stand out against new construction and other listings.

- For buyers: Get pre‑approved, consider rate‑lock options when rates are favorable, and use inspection and financing contingencies to protect your purchase. Prioritize neighborhoods with strong schools and commute times if family needs and privacy are a priority.

- For both: Work with a local agent who can provide up‑to‑date information on nearby listings, recent sales, and specific St. Louis districts or neighborhoods you’re targeting.

Key numbers at a glance (verify with latest NAR/MLS reports)

- Median sale‑to‑list price: typically high but easing vs. last year (example: ~98–100% in many metros).

- Median days on market: increased modestly vs. 2025 in several markets.

- Months‑of‑supply: still low overall but up slightly from last year, signaling a small shift toward balance.

- Mortgage rates: remain a major factor for buyers’ affordability and offer timelines.

Need local details? Contact a St. Louis agent for neighborhood‑level listings, school district information, and tailored guidance on whether to list now or wait for a better market window.

FAQ (short)

- Q: Is now a good time to sell? A: If your home is well priced and prepared, sellers can still achieve strong results, though timing and pricing need to be more strategic than in 2024.

- Q: Should buyers wait? A: Waiting for lower rates may help, but buyers who find a well‑priced single-family home in the right neighborhood and lock a favorable rate can still get good long‑term value.